Table of Contents

1. 1977 Letter

2. 1978 Letter

3. 1979 Letter

4. 1980 Letter

5. 1981 Letter

This issue does not and is not meant to fully summarize or recap the Berkshire Hathaway shareholder letters. Rather, it includes the tidbits I found interesting and wanted to highlight during my reading. Always do your own reading and come to your own conclusions about Mr. Buffett’s opinions.

How to find the quotations: It is difficult to cite specific sections of a given letter because there are no consistent page numbers and the sections are not numbered. The easiest way to find the quote is to open a PDF of the letter and use the search feature.

1. 1977 Berkshire Hathaway Letter, dated March 14, 1978

- Major World Events Wiki for 1977

- S&P 500 Trajectory (inflation-adjusted): downward, from about 440 to 370

- Inflation: 6.5%

- Interest Rate on a 30-year fixed-rate mortgage: 8.8%

- US President: Gerald Ford went out in Jan 1977, and Jimmy Carter came in.

1977 Letter in PDF from Berkshire Hathaway website

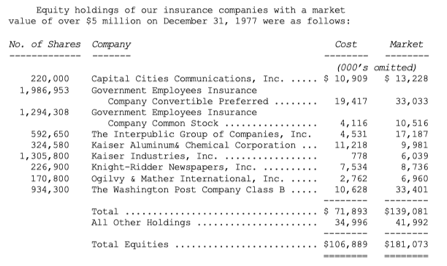

Major Berkshire investments reported in the letter:

Notable: Capital Cities was television – eventually became the network ABC. The second and third ones on the list are GEICO Insurance.

Standard of success mentioned at the beginning: operating earnings.

Highlights:

- In this first letter Mr. Buffett put up on Berkshire’s website, he didn’t make any huge pronouncements or comment much on larger economics or investing. I’ve gotten used to those sorts of things in his contemporary letters, but back then, he was focused on straightforward accounting and management. He wanted his shareholders to know exactly what was happening in that company, and who was making the decisions. His overall message was that while the textile business was slowly failing, and was not going to get better, the other parts of Berkshire Hathaway, especially the insurance business, was doing well and was well-stewarded.

- Berkshire had already been a public company for a long time. Buffett came in and made changes to it, moving away from textiles and towards insurance and investing, and I see this letter as him trying to thread the needle between saying “hey investors, I’m not a weirdo who came in to change this whole thing up” and “actually not really guys, the textile industry is dying and we’re making some changes over here.”

Checklist points:

- “we believe a more appropriate measure of managerial economic performance to be return on equity capital.” (4th paragraph) He measures managers of the business on their return on equity.

- In “Insurance Underwriting” 1st paragraph: “No additional shares of Berkshire Hathaway stock have been issued to achieve any of this growth.” This is going straight to my checklist – it’s one thing to make a purchase with stock, but it’s entirely another to issue new shares and dilute existing shareholders to make a purchase.

- Tailwinds, rather than headwinds. For my comfort. “It is comforting to be in a business where some mistakes can be made and yet a quite satisfactory overall performance can be achieved. In a sense, this is the opposite case from our textile business where even very good management probably can average only modest results. One of the lessons your management has learned – and, unfortunately, sometimes re-learned – is the importance of being in businesses where tailwinds prevail rather than headwinds.”

Particular points of candor:

- “The textile business again had a very poor year in 1977. We have mistakenly predicted better results in each of the last two years. This may say something about our forecasting abilities, the nature of the textile industry, or both.”

- He straight up said that he’s keeping the textile business open because, his number one reason, Berkshire employs older people with non-transferable skills who work with management to continue to maintain a viable operation. In other words, this business is barely eking by, but we want to keep these people employed as long as possible. Talk to me about Buffett not being an icon of ESG again?

I was also struck by:

- In the very first paragraph, he made the point that single-year capital losses or gains are not significant. He has never wavered from this stance that a single year’s results don’t tell you much. The same from the very beginning. Love it.

- Over and over, he stated the names of people vital to the success of the business. He gave credit out, publicly and repeatedly, in this document that has lived for over forty years. That’s quite different from a shout-out on an earnings call.

- “We select our marketable equity securities in much the same way we would evaluate a business for acquisition in its entirety. We want the business to be (1) one that we can understand, (2) with favorable long-term prospects, (3) operated by honest and competent people, and (4) available at a very attractive price. We ordinarily make no attempt to buy equities for anticipated favorable stock price behavior in the short term. In fact, if their business experience continues to satisfy us, we welcome lower market prices of stocks we own as an opportunity to acquire even more of a good thing at a better price.” Oh my gosh – this is the checklist I based my book on, but years earlier. Clearly this is a talked-about checklist for them. Beautiful.

2. 1978 Letter, dated March 26, 1979

- Major World Events Wiki for 1978

- S&P 500 Trajectory (inflation-adjusted): flat, popping around 400

- Inflation: 7.6%

- Interest Rate on a 30-year fixed-rate mortgage: 9.6%

- US President: Jimmy Carter

1978 Letter in PDF from Berkshire Hathaway website

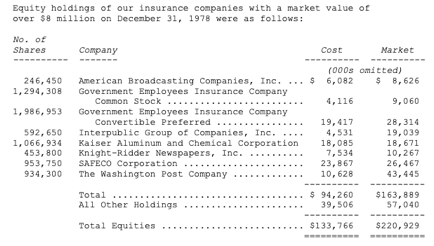

Major Berkshire investments reported in the letter:

Standard of success mentioned at the beginning: operating earnings, and long-term growth in equity per share. He notes equity per share growth from all sources, and from operating earnings only.

Highlights:

- This letter was entirely focused on the activities of Berkshire’s business. Which is not notable – except that after this letter, he moved more towards larger economic issues, comments on accounting and evaluating businesses in general, and the choices made at other companies. In contrast, this letter was probably the last one focused only on Berkshire’s internal world.

- “There were equities of identifiably excellent companies available – but very few at interesting prices. (An irresistible footnote: in 1971, pension fund managers invested a record 122% of net funds available in equities – at full prices they couldn’t buy enough of them. In 1974, after the bottom had fallen out, they committed a then record low of 21% to stocks.)”

- Sound familiar to today? At full prices people can’t buy enough stocks, and it’s obvious what will happen if they start to fall again and government can’t intervene.

- I thought this was interesting: “And consistent attractive purchasing is likely to prove to be of more eventual benefit to us than any selling opportunities provided by a short-term run up in stock prices to levels at which we are unwilling to continue buying.”

Checklist points:

- “our purchase of SAFECO was made at substantially under book value. We paid less than 100 cents on the dollar for the best company in the business, when far more than 100 cents on the dollar is being paid for mediocre companies in corporate transactions. And there is no way to start a new operation – with necessarily uncertain prospects – at less than 100 cents on the dollar.”

- My takeaways: (1) check book value – sounds obvious, but prices these days are so divorced from book value that it gets overlooked, and important but overlooked is exactly the sort of thing that must go on a checklist, and (2) run the thought process of how a brand-new company or division of an existing company could compete with this company, and how much would it cost them to do so?

- Basically, trust a tightly-run operation a little more. “Our experience has been that the manager of an already highcost operation frequently is uncommonly resourceful in finding new ways to add to overhead, while the manager of a tightly-run operation usually continues to find additional methods to curtail costs, even when his costs are already well below those of his competitors.”

Particular points of candor:

- “We continue to look for ways to expand our insurance operation. But your reaction to this intent should not be unrestrained joy. Some of our expansion efforts – largely initiated by your Chairman have been lackluster, others have been expensive failures.”

- Preach! “Of course, with a minor interest we do not have the right to direct or even influence management policies of SAFECO. But why should we wish to do this? The record would indicate that they do a better job of managing their operations than we could do ourselves. While there may be less excitement and prestige in sitting back and letting others do the work, we think that is all one loses by accepting a passive participation in excellent management. Because, quite clearly, if one controlled a company run as well as SAFECO, the proper policy also would be to sit back and let management do its job.”

I was also struck by:

- Again, like last year’s, named the people who achieved the success. So many names!

- Especially this epic closing: “Associated’s business has not grown, and it consistently has faced adverse demographic and retailing trends. But Ben’s combination of merchandising, real estate and cost-containment skills has produced an outstanding record of profitability, with returns on capital necessarily employed in the business often in the 20% after-tax area. Ben is now 75 and, like Gene Abegg, 81, at Illinois National and Louie Vincenti, 73, at Wesco, continues daily to bring an almost passionately proprietary attitude to the business. This group of top managers must appear to an outsider to be an overreaction on our part to an OEO bulletin on age discrimination. While unorthodox, these relationships have been exceptionally rewarding, both financially and personally. It is a real pleasure to work with managers who enjoy coming to work each morning and, once there, instinctively and unerringly think like owners. We are associated with some of the very best.”

- And, again, the famous checklist points: “We get excited enough to commit a big percentage of insurance company net worth to equities only when we find (1) businesses we can understand, (2) with favorable long-term prospects, (3) operated by honest and competent people, and (4) priced very attractively. We usually can identify a small number of potential investments meeting requirements (1), (2) and (3), but (4) often prevents action.”

3. 1979 Letter, dated March 3, 1980

- Major World Events Wiki for 1979

- S&P 500 Trajectory (inflation-adjusted): downward, from about 440 to 370

- Inflation: 11.2% – steep rise from last year’s 8ish%

- Interest Rate on a 30-year fixed-rate mortgage: 11.20%

- US President: Jimmy Carter

1979 Letter in PDF from Berkshire Hathaway website

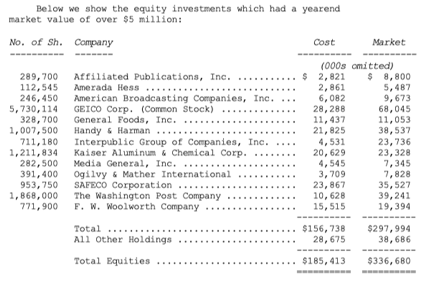

Major Berkshire investments reported in the letter:

Standard of success mentioned at the beginning: Operating earnings return on equity. “We continue to feel that the ratio of operating earnings (before securities gains or losses) to shareholders’ equity with all securities valued at cost is the most appropriate way to measure any single year’s operating performance.” (emphasis Buffett’s)

Highlights:

- This letter felt to me like it was about uncertainty in the face of rising inflation. Would it keep going? Would it abate? He went into it but also gave a lot of time to long-term investing evaluations.

- Mr. Buffett got into the effects of inflation rising so dramatically in the second half of “Long Term Results”. It directly affects the purchasing power gain of any stock gains. “We have no corporate solution to this problem; high inflation rates will not help us earn higher rates of return on equity….We intend to continue to do as well as we can in managing the internal affairs of the business. But you should understand that external conditions affecting the stability of currency may very well be the most important factor in determining whether there are any real rewards from your investment in Berkshire Hathaway.”

- Wow. Inflation was so bad, he wasn’t even sure if paper currency in its contemporary value would hold up for 30 years. “We have severe doubts as to whether a very long-term fixedinterest bond, denominated in dollars, remains an appropriate business contract in a world where the value of dollars seems almost certain to shrink by the day. Those dollars, as well as paper creations of other governments, simply may have too many structural weaknesses to appropriately serve as a unit of long term commercial reference. If so, really long bonds may turn out to be obsolete instruments and insurers who have bought those maturities of 2010 or 2020 could have major and continuing problems on their hands.” (my emphasis) That is severe doubt about the future. I note his attitude is markedly one of doubt, not of fear.

Checklist points:

- To evaluate managers, I thought this was really interesting: “The primary test of managerial economic performance is the achievement of a high earnings rate on equity capital employed (without undue leverage, accounting gimmickry, etc.) and not the achievement of consistent gains in earnings per share.” (emphasis mine.) He’s saying there are other reasons earnings can rise than the performance of an executive. He went to push the point: “In our view, many businesses would be better understood by their shareholder owners, as well as the general public, if managements and financial analysts modified the primary emphasis they place upon earnings per share, and upon yearly changes in that figure.”

- Just because the numbers make it seem like a great bargain of a stock, is the hill it has to climb STILL too steep? “Your Chairman made the decision a few years ago to purchase Waumbec Mills in Manchester, New Hampshire, thereby expanding our textile commitment. By any statistical test, the purchase price was an extraordinary bargain; we bought well below the working capital of the business and, in effect, got very substantial amounts of machinery and real estate for less than nothing. But the purchase was a mistake. While we labored mightily, new problems arose as fast as old problems were tamed. Both our operating and investment experience cause us to conclude that “turnarounds” seldom turn, and that the same energies and talent are much better employed in a good business purchased at a fair price than in a poor business purchased at a bargain price.”

Particular points of candor:

- “We had substantially more capital to work with in 1979 than in 1978, and our performance in utilizing that capital fell short of the earlier year, even though per-share earnings rose.” I mean. It’s easy to obfuscate poor performance if earnings rose, but nope, he called himself out. There is no one out there who does this except him. I wish there were others.

- I have literally printed the following out, and put it on my bulletin board so I see it at all times. “We currently believe that equity markets in 1980 are likely to evolve in a manner that will result in an underperformance by our portfolio for the first time in recent years. We very much like the companies in which we have major investments, and plan no changes to try to attune ourselves to the markets of a specific year.” Anticipate underperformance in the stock of a company I still like? Plan no changes. Got it.

I was also struck by:

- Quarterly reports are narrative-free because there’s no meaningful info of long-term significance on such a short term. Shareholders, as owners, should get he same sort of reporting as the managers of the business: long-term, meaningful, and directly from the people running the business. Other companies communicate differently, and often via PR employees. I thought this nailed it, and it’s gotten me thinking about the companies I own: “In large part, companies obtain the shareholder constituency that they seek and deserve. If they focus their thinking and communications on short-term results or short-term stock market consequences they will, in large part, attract shareholders who focus on the same factors. And if they are cynical in their treatment of investors, eventually that cynicism is highly likely to be returned by the investment community.”

- In which category are the companies I own?

- Phil Fisher! Got to read his book. Mr. Buffett went on, to hammer home the point that we can’t have a company simultaneously focused on short-term stock price and long-term stability. “Phil Fisher, a respected investor and author, once likened the policies of the corporation in attracting shareholders to those of a restaurant attracting potential customers. A restaurant could seek a given clientele – patrons of fast foods, elegant dining, Oriental food, etc. – and eventually obtain an appropriate group of devotees. If the job were expertly done, that clientele, pleased with the service, menu, and price level offered, would return consistently. But the restaurant could not change its character constantly and end up with a happy and stable clientele. If the business vacillated between French cuisine and take-out chicken, the result would be a revolving door of confused and dissatisfied customers. So it is with corporations and the shareholder constituency they seek. You can’t be all things to all men, simultaneously seeking different owners whose primary interests run from high current yield to long-term capital growth to stock market pyrotechnics, etc.” (emphasis mine)

4. 1980 Letter, dated February 27, 1981

- Major World Events Wiki for 1980

- S&P 500 Trajectory (inflation-adjusted): downward, from about 440 to 370

- Inflation: 13.5% (oh my gosh!)

- Interest Rate on a 30-year fixed-rate mortgage: 13.74%

- US President: Jimmy Carter

1980 Letter in PDF from Berkshire Hathaway website

Major Berkshire investments reported in the letter:

Standard of success mentioned at the beginning: operating earnings and return on beginning equity capital.

Highlights:

- This letter is about inflation. Super interesting. It’s now the second year of high inflation and he clearly has it foremost in his mind.

- He went deeply into how Berkshire does accounting for its partially-owned businesses.

- What the heck is he talking about in this little aside? Salt? Magnesium? I don’t know, and my quick internet searching turned up nothing, but I appreciate the joke. “In the sixteen years since present management assumed responsibility for Berkshire, book value per share with insurance-held equities valued at market has increased from $19.46 to $400.80, or 20.5% compounded annually. (You’ve done better: the value of the mineral content in the human body compounded at 22% annually during the past decade.)”

Checklist points:

- In his opening paragraph, he included an interesting nuance that I’ve marked for my checklist to make sure I understand them for a given company. [my emphasis added] “We believe the latter yardstick to be the most appropriate measure of single-year managerial economic performance. Informed use of that yardstick, however, requires an understanding of many factors, including accounting policies, historical carrying values of assets, financial leverage, and industry conditions.”

- “Our insurance companies will continue to make large investments in well-run, favorably-situated…” Well-run. Favorably-situated.

- Inflation check. “For capital to be truly indexed, return on equity must rise, i.e., business earnings consistently must increase in proportion to the increase in the price level without any need for the business to add to capital – including working capital employed. (Increased earnings produced by increased investment don’t count.) Only a few businesses come close to exhibiting this ability. And Berkshire Hathaway isn’t one of them.”

- Tidbit on dividends, which is a good reminder to me as an investor – don’t fall into what I call the Dividend Contract of Expectations, in which steadily growing dividends may falsely imply a company is financially healthy. “But, while our reported operating earnings reflect only the dividends received from such companies, our economic well-being is determined by their earnings, not their dividends.”

- “GEICO represents the best of all investment worlds – the coupling of a very important and very hard to duplicate business advantage with an extraordinary management whose skills in operations are matched by skills in capital allocation.”

- Description of an Event that is not systemic and is fixable, and totally different than a turnaround. In “GEICO Corp.” section. “GEICO was designed to be the low-cost operation in an enormous marketplace (auto insurance) populated largely by companies whose marketing structures restricted adaptation. Run as designed, it could offer unusual value to its customers while earning unusual returns for itself. For decades it had been run in just this manner. Its troubles in the mid-70s were not produced by any diminution or disappearance of this essential economic advantage. GEICO’s problems at that time put it in a position analogous to that of American Express in 1964 following the salad oil scandal. Both were one-of-a-kind companies, temporarily reeling from the effects of a fiscal blow that did not destroy their exceptional underlying economics. The GEICO and American Express situations, extraordinary business franchises with a localized excisable cancer (needing, to be sure, a skilled surgeon), should be distinguished from the true “turnaround” situation in which the managers expect – and need – to pull off a corporate Pygmalion.”

- “Right behind having financial problems yourself, the next worst plight is to have a large group of competitors with financial problems that they can defer by a “sell-at-any-price” policy.”

On inflation:

- Inflation and interest rates were as high as they’ve ever been (and turned out it was as high as it would go). Clearly, inflation was the dominant topic of the day, and Buffett devoted most of his letter to parsing out its effects on investments.

- Very educational for us, when we may be facing much higher inflation soon.

- The section to read on inflation is “Results for Owners”. If you skim this letter, I recommend reading this section a bit more slowly. It’s an inflation education.

- “Unfortunately, earnings reported in corporate financial statements are no longer the dominant variable that determines whether there are any real earnings for you, the owner. For only gains in purchasing power represent real earnings on investment.”

- Inflation creates a hurdle rate over which a company must make a return on equity, in order to make any real return for its shareholders. He describes it as running up a down escalator. In 1980 the inflation rate, the hurdle rate, was 13%. The idea really struck me, because when we see a company these days that is making a 13% return on equity, that’s pretty good. But in a world of high inflation and short-term stockholdings, it’s actually not even keeping up. He explained:

- “For example, in a world of 12% inflation a business earning 20% on equity (which very few manage consistently to do) and distributing it all to individuals in the 50% bracket is chewing up their real capital, not enhancing it. (Half of the 20% will go for income tax; the remaining 10% leaves the owners of the business with only 98% of the purchasing power they possessed at the start of the year – even though they have not spent a penny of their “earnings”).”

- The only solution is being indexed to inflation, he says. “For capital to be truly indexed, return on equity must rise, i.e., business earnings consistently must increase in proportion to the increase in the price level without any need for the business to add to capital – including working capital employed. (Increased earnings produced by increased investment don’t count.) Only a few businesses come close to exhibiting this ability. And Berkshire Hathaway isn’t one of them.” So which ones are??? I’ve put this on my checklist and it’s probably the most enigmatic addition.

- Looking for companies that convert earnings into pure cash, without putting more and more of that cash back into the business. “As inflation intensifies, more and more companies find that they must spend all funds they generate internally just to maintain their existing physical volume of business. There is a certain miragelike quality to such operations. However attractive the earnings numbers, we remain leery of businesses that never seem able to convert such pretty numbers into no-strings-attached cash.”

Particular points of candor:

- “…we have a much larger economic interest in the aluminum business than in practically any of the operating businesses we control and on which we report in more detail. If we maintain our holdings, our long-term performance will be more affected by the future economics of the aluminum industry than it will by direct operating decisions we make concerning most companies over which we exercise managerial control.” No other CEO would point out this exposure. They’d happily hide the risk.

I was also struck by:

His beautiful epitaph for Gene Abegg at the end of the letter.

- Never have I read a better description of a purchase transaction’s pitfalls. “You learn a great deal about a person when you purchase a business from him and he then stays on to run it as an employee rather than as an owner. Before the purchase the seller knows the business intimately, whereas you start from scratch. The seller has dozens of opportunities to mislead the buyer – through omissions, ambiguities, and misdirection. After the check has changed hands, subtle (and not so subtle) changes of attitude can occur and implicit understandings can evaporate. As in the courtship-marriage sequence, disappointments are not infrequent.”

- He wrote that Gene shot straight, would add items of value previously unmentioned, and never forgot he was handling other people’s money at his bank. But more so: “Dozens of Rockford citizens have told me over the years of help Gene extended to them. In some cases this help was financial; in all cases it involved much wisdom, empathy and friendship.” May such good things be said about each of us.

5. 1981 Letter, dated February 26, 1982

- Major World Events Wiki for 1981

- S&P 500 Trajectory (inflation-adjusted): downward, from about 440 to 370

- Inflation: 10.3%, down a bit from last year’s high

- Interest Rate on a 30-year fixed-rate mortgage: 16.63%, higher than last year

- US President: Jimmy Carter out, Ronald Reagan inaugurated just before this letter

1981 Letter in PDF from Berkshire Hathaway website

Major Berkshire investments reported in the letter:

Notable: Quite a few changes from last year.

Standard of success mentioned at the beginning: operating earnings and return on beginning equity capital with securities valued at cost. “

Highlights:

- This letter is about acquisitions. Their wisdom, and lack thereof. There must have been a lot of buying/selling at that time, because he launched into discussing acquisitions very early in the letter, and he clearly thinks a lot of buying is being done for short-term, bad, reasons: (1) CEOs are bored, (2) CEOs want their companies to be bigger because it makes them feel more important, and/or (3) CEOs have an inflated opinion of their effect on the purchased company. Phew. That’s a proper Buffett burn.

- I’d add that these days, CEOs still want their companies to be bigger so they feel important, but instead of accomplishing that through acquisition they do so through share buybacks.

- The best kind of company is “Category 1” – inflation-adapted: “Such favored business must have two characteristics: (1) an ability to increase prices rather easily (even when product demand is flat and capacity is not fully utilized) without fear of significant loss of either market share or unit volume, and (2) an ability to accommodate large dollar volume increases in business (often produced more by inflation than by real growth) with only minor additional investment of capital. Managers of ordinary ability, focusing solely on acquisition possibilities meeting these tests, have achieved excellent results in recent decades.”

- The ideal is that kind of company, bought by a managerial superstar, who can identify the companies above and make them better. (He calls a company run by a managerial superstar Category 2.)

- These are the kind of companies to look for as we go towards inflation, but also anytime. These are just great companies.

- Price. What’s ok? He says, “We will continue to seek the acquisition of businesses in their entirety at prices that will make sense, even should the future of the acquired enterprise develop much along the lines of its past. We may very well pay a fairly fancy price for a Category 1 business if we are reasonably confident of what we are getting.” A “fairly fancy price” is quite interesting, considering that we need to make sure we keep a margin of safety, but he’s clearly said that, at least back in 1981, he thought it was ok to pay a little more for such an exceptional company.

- Inflation. He referred to “the unrelenting destruction of currency values…” Oof. I can feel the frustration.

- Deep dive into whether equity – stocks, companies – really add value, espeically against the powerful headwind of inflation. This comment on change has stuck with me: “It is much easier for investors to utilize historic p/e ratios or for managers to utilize historic business valuation yardsticks than it is for either group to rethink their premises daily. When change is slow, constant rethinking is actually undesirable; it achieves little and slows response time. But when change is great, yesterday’s assumptions can be retained only at great cost. And the pace of economic change has become breathtaking.” (emphasis mine) I think right now, change is great.

Checklist points:

- These are THE mistakes an investor can make. “We expect that undistributed earnings from such companies will produce full value (subject to tax when realized) for Berkshire and its shareholders. If they don’t, we have made mistakes as to either: (1) the management we have elected to join; (2) the future economics of the business; or (3) the price we have paid.”

- And then he goes on: “Category (2) miscalculations are the most common. Of course, it is necessary to dig deep into our history to find illustrations of such mistakes – sometimes as deep as two or three months back. For example, last year your Chairman volunteered his expert opinion on the rosy future of the aluminum business. Several minor adjustments to that opinion – now aggregating approximately 180 degrees – have since been required.” Two or three months back…I love him.

Particular points of candor:

- Ooohhh. “Your Chairman, unfortunately, does not qualify for Category 2 [the managerial superstar category]. And, despite a reasonably good understanding of the economic factors compelling concentration in Category 1 [the inflation-adapted company category], our actual acquisition activity in that category has been sporadic and inadequate. Our preaching was better than our performance. (We neglected the Noah principle: predicting rain doesn’t count, building arks does.)” Predicting rain doesn’t count. Building arks does. I feel this one in my bones.

- “…inflation acts as a gigantic corporate tapeworm. That tapeworm preemptively consumes its requisite daily diet of investment dollars regardless of the health of the host organism. Whatever the level of reported profits (even if nil), more dollars for receivables, inventory and fixed assets are continuously required by the business in order to merely match the unit volume of the previous year. The less prosperous the enterprise, the greater the proportion of available sustenance claimed by the tapeworm.”

- ““Forecasts”, said Sam Goldwyn, “are dangerous, particularly those about the future.” (Berkshire shareholders may have reached a similar conclusion after rereading our past annual reports featuring your Chairman’s prescient analysis of textile prospects.)”

I was also struck by:

- Funny, it’s opposite today. “Small portions of exceptionally good businesses are usually available in the securities markets at reasonable prices. But such businesses are available for purchase in their entirety only rarely, and then almost always at high prices.”

- He’s very proud of Berkshire’s corporate charitable contribution program, in which shareholders may choose where gifts shall be made. It’s very sweet.